EMD Trend [InvestorUnknown]EMD Trend is a dynamic trend-following indicator that utilizes Exponential Moving Deviation (EMD) to build adaptive channels around a selected moving average. Designed for traders who value responsive trend signals with built-in volatility sensitivity, this tool highlights directional bias, market regime shifts, and potential breakout opportunities.

How It Works

Instead of using standard deviation, EMD Trend employs the exponential moving average of the absolute deviation from a moving average—producing smoother, faster-reacting upper and lower bounds:

Bullish (Risk-ON Long): Price crosses above the upper EMD band

Bearish (Risk-ON Short): Price crosses below the lower EMD band

Neutral: Price stays within the channel, indicating potential mean reversion or low momentum

Trend direction is defined by price interaction with these bands, and visual cues (color-coded bars and fills) help quickly identify market conditions.

Features

7 Moving Average Types: SMA, EMA, HMA, DEMA, TEMA, RMA, FRAMA

Custom Price Source: Choose close, hl2, ohlc4, or others

EMD Multiplier: Controls the width of the deviation envelope

Bar Coloring: Candles change color based on current trend

Intra-bar Signal Option: Enables faster updates (with optional repainting)

Speculative Zones: Fills highlight aggressive momentum moves beyond EMD bounds

Backtest Mode

Switch to Backtest Mode for performance evaluation over historical data:

Equity Curve Plot: Compare EMD Trend strategy vs. Buy & Hold

Trade Metrics Table: View number of trades, win/loss stats, profits

Performance Metrics Table: Includes CAGR, Sharpe, max drawdown, and more

Custom Start Date: Select from which date the backtest should begin

Trade Sizing: Configure capital and trade percentage per entry

Signal Filters: Choose from Long Only, Short Only, or Both

Alerts

Built-in alerts let you automate entries, exits, and trend transitions:

LONG (EMD Trend) - Trend flips to Long

SHORT (EMD Trend) - Trend flips to Short

RISK-ON LONG - Price crosses above upper EMD band

RISK-OFF LONG - Price crosses back below upper EMD band

RISK-ON SHORT - Price crosses below lower EMD band

RISK-OFF SHORT - Price crosses back above lower EMD band

Use Cases

Trend Confirmation with volatility-sensitive boundaries

Momentum Entry Filtering via breakout zones

Mean Reversion Avoidance in sideways markets

Backtesting & Strategy Building with real-time metrics

Disclaimer

This indicator is intended for informational and educational purposes only. It does not constitute investment advice. Historical performance does not guarantee future results. Always backtest and use in simulation before live trading.

" TABLE "に関するスクリプトを検索

RMSD Trend [InvestorUnknown]RMSD Trend is a trend-following indicator that utilizes Root Mean Square Deviation (RMSD) to dynamically construct a volatility-weighted trend channel around a selected moving average. This indicator is designed to enhance signal clarity, minimize noise, and offer quantitative insights into market momentum, ideal for both discretionary and systematic traders.

How It Works

At its core, RMSD Trend calculates a deviation band around a selected moving average using the Root Mean Square Deviation (similar to standard deviation but with squared errors), capturing the magnitude of price dispersion over a user-defined period. The logic is simple:

When price crosses above the upper deviation band, the market is considered bullish (Risk-ON Long).

When price crosses below the lower deviation band, the market is considered bearish (Risk-ON Short).

If price stays within the band, the market is interpreted as neutral or ranging, offering low-risk decision zones.

The indicator also generates trend flips (Long/Short) based on crossovers and crossunders of the price and the RMSD bands, and colors candles accordingly for enhanced visual feedback.

Features

7 Moving Average Types: Choose between SMA, EMA, HMA, DEMA, TEMA, RMA, and FRAMA for flexibility.

Customizable Source Input: Use price types like close, hl2, ohlc4, etc.

Volatility-Aware Channel: Adjustable RMSD multiplier determines band width based on volatility.

Smart Coloring: Candles and bands adapt their colors to reflect trend direction (green for bullish, red for bearish).

Intra-bar Repainting Toggle: Option to allow more responsive but repaintable signals.

Speculation Fill Zones: When price exceeds the deviation channel, a semi-transparent fill highlights potential momentum surges.

Backtest Mode

Switching to Backtest Mode unlocks a robust suite of simulation features:

Built-in Equity Curve: Visualizes both strategy equity and Buy & Hold performance.

Trade Metrics Table: Displays the number of trades, win rates, gross profits/losses, and long/short breakdowns.

Performance Metrics Table: Includes key stats like CAGR, drawdown, Sharpe ratio, and more.

Custom Date Range: Set a custom start date for your backtest.

Trade Sizing: Simulate results using position sizing and initial capital settings.

Signal Filters: Choose between Long & Short, Long Only, or Short Only strategies.

Alerts

The RMSD Trend includes six built-in alert conditions:

LONG (RMSD Trend) - Trend flips from Short to Long

SHORT (RMSD Trend) - Trend flips from Long to Short

RISK-ON LONG (RMSD Trend) - Price crosses above upper RMSD band

RISK-OFF LONG (RMSD Trend) - Price falls back below upper RMSD band

RISK-ON SHORT (RMSD Trend) - Price crosses below lower RMSD band

RISK-OFF SHORT (RMSD Trend) - Price rises back above lower RMSD band

Use Cases

Trend Confirmation: Confirms directional bias with RMSD-weighted confidence zones.

Breakout Detection: Highlights moments when price breaks free from historical volatility norms.

Mean Reversion Filtering: Avoids false signals by incorporating RMSD’s volatility sensitivity.

Strategy Development: Backtest your signals or integrate with a broader system for alpha generation.

Settings Summary

Display Mode: Overlay (default) or Backtest Mode

Average Type: Choose from SMA, EMA, HMA, DEMA, etc.

Average Length: Lookback window for moving average

RMSD Multiplier: Band width control based on RMS deviation

Source: Input price source (close, hl2, ohlc4, etc.)

Intra-bar Updating: Real-time updates (may repaint)

Color Bars: Toggle bar coloring by trend direction

Disclaimer

This indicator is provided for educational and informational purposes only. It is not financial advice. Past performance, including backtest results, is not indicative of future results. Use with caution and always test thoroughly before live deployment.

OrderFlow Sentiment SwiftEdgeOrderFlow Sentiment SwiftEdge

Overview

OrderFlow Sentiment SwiftEdge is a visual indicator designed to help traders analyze market dynamics through a simulated orderbook and market sentiment display. It breaks down the current candlestick into 10 price bins, estimating buy and sell volumes, and presents this data in an orderbook table alongside a sentiment row showing the buy vs. sell bias. This tool provides a quick and intuitive way to assess orderflow activity and market sentiment directly on your chart.

How It Works

The indicator consists of two main components: an Orderbook Table and a Market Sentiment Row.

Orderbook Table:

Simulates buy and sell volumes for the current candlestick by distributing total volume into 10 price bins based on price movement and proximity to open/close levels.

Displays the price bins in a table with columns for Price, Buy Volume, and Sell Volume, sorted from highest to lowest price.

Highlights the current price level in orange for easy identification, while buy and sell dominance is indicated with green (buy) or red (sell) backgrounds.

Market Sentiment Row:

Calculates the overall buy and sell sentiment (as a percentage) for the current candlestick based on the simulated orderflow data.

Displays the sentiment above the orderbook table, with the background colored green if buyers dominate or red if sellers dominate.

Features

Customizable Colors: Choose colors for buy (default: green), sell (default: red), and current price (default: orange) levels.

Lot Scaling Factor: Adjust the volume scaling factor (default: 0.1 lots per volume unit) to simulate realistic lot sizes.

Table Position: Select the table position on the chart (Top, Middle, or Bottom; default: Middle).

Default Properties

Positive Color: Green

Negative Color: Red

Current Price Color: Orange

Lot Scaling Factor: 0.1

Table Position: Middle

Usage

This indicator is ideal for traders who want to visualize orderflow dynamics and market sentiment in real-time. The orderbook table provides a snapshot of buy and sell activity at different price levels within the current candlestick, helping you identify areas of high buying or selling pressure. The sentiment row offers a quick overview of market bias, allowing you to gauge whether buyers or sellers are currently dominating. Use this information to complement your trading decisions, such as identifying potential breakout levels or confirming trend direction.

Limitations

This indicator simulates orderflow data based on candlestick price movement and volume, as TradingView does not provide tick-by-tick data. The volume distribution is an approximation and should be used as a visual aid rather than a definitive measure of market activity.

The indicator operates on the chart's current timeframe and does not incorporate higher timeframe data.

The simulated volumes are scaled using a user-defined lot scaling factor, which may not reflect actual market lot sizes.

Disclaimer

This indicator is for informational purposes only and does not guarantee trading results. Always conduct your own analysis and manage risk appropriately. The simulated orderflow data is an estimation and may not reflect real market conditions.

ETF Builder & Backtest System [TradeDots]Create, analyze, and monitor your own custom “ETF-like” portfolio directly on TradingView. This script merges up to 10 different assets with user-defined weightings into a single composite chart, allowing you to see how your personalized portfolio would have performed historically. It is an original tool designed to help traders and investors quickly gauge risk and return profiles without leaving the TradingView platform.

📝 HOW IT WORKS

1. Custom Portfolio Construction

Multiple Assets : Combine up to 10 different stocks, ETFs, cryptocurrencies, or other symbols.

User-Defined Weights : Allocate each asset a percentage weight (e.g., 15% in AAPL, 10% in MSFT, etc.).

Single Composite Value : The script calculates a weighted “ETF-style” price, effectively simulating a merged portfolio curve on your chart.

2. Performance Tracking & Return Analysis

Automatic History Capture : The indicator records each asset’s starting price when it first appears in your chosen date range.

Rolling Updates : As time progresses, all asset prices are continually evaluated and the portfolio value is updated in real time.

Buy & Hold Returns : See how each asset—and the overall portfolio—performed from the “start” date to the most recent bar.

Annualized Return : Automatically calculates CAGR (Compound Annual Growth Rate) to help visualize performance over varying timescales.

3. Table & Visual Output

Performance Table : A comprehensive table displays individual asset returns, annualized returns, and portfolio totals.

Normalized Chart Plot : The composite ETF value is scaled to 100 at the start date, making it easy to compare relative growth or decline.

Optional Time Filter : You can define a specific date range (Start/End Dates) to focus on a particular period or to limit historical data.

⚙️ KEY FEATURES

1. Flexible Asset Selection

Choose any symbols from multiple asset classes. The script will only run calculations when data is available—no need to worry about missing quotes.

2. Dynamic Table Reporting

Start Price for each asset

Percentage Weight in the portfolio

Total Return (%) and Annualized Return (%)

3. Simple Backtesting Logic

This script takes a straightforward Buy & Hold perspective. Once the start date is reached, the portfolio remains static until the end date, so you can quickly assess hypothetical growth.

4. Plot Customization

Toggle the main “ETF” plot on/off.

Alter the visual style for tables and text.

Adjust the time filter to limit or extend your performance measurement window.

🚀 HOW TO USE IT

1. Add the Script

Search for “ETF Builder & Backtest System ” in the Indicators & Strategies tab or manually add it to your chart after saving it in your Pine Editor.

2. Configure Inputs

Enable Time Filter : Choose whether to restrict the analysis to a particular date range.

Start & End Date : Define the period you want to measure performance over (e.g., from 2019-12-31 to 2025-01-01).

Assets & Weights : Enter each symbol and specify a percentage weight (up to 10 assets).

Display Options : Pick where you want the Table to appear and choose background/text colors.

3. Interpret the Table & Plots

Asset Rows : Each asset’s ticker, weighting, start price, and performance metrics.

ETF Total Row : Summarizes total weighting, composite starting value, and overall returns.

Normalized Plot : Tracks growth/decline of the combined portfolio, starting at 100 on the chart.

4. Refine Your Strategy

Compare how different weights or a new mix of assets would have performed over the same period.

Assess if certain assets contribute disproportionately to your returns or volatility.

Use the results to guide allocations in your real trading or paper trading accounts.

❗️LIMITATIONS

1. Buy & Hold Only

This script does not handle rebalancing or partial divestments. Once the portfolio starts, weights remain fixed throughout the chosen timeframe.

2. No Reinvestment Tracking

Dividends or other distributions are not factored into performance.

3. Data Availability

If historical data for a particular asset is unavailable on TradingView, related results may display as “N/A.”

4. Market Regimes & Volatility

Past performance does not guarantee similar future behavior. Markets can change rapidly, which may render historical backtests less predictive over time.

⚠️ RISK DISCLAIMER

Trading and investing carry significant risk and can result in financial loss. The “ETF Builder & Backtest System ” is provided for informational and educational purposes only. It does not constitute financial advice.

Always conduct your own research.

Use proper risk management and position sizing.

Past performance does not guarantee future results.

This script is an original creation by TradeDots, published under the Mozilla Public License 2.0.

Use this indicator as part of a broader trading or investment approach—consider fundamental and technical factors, overall market context, and personal risk tolerance. No trading tool can assure profits; exercise caution and responsibility in all financial decisions.

RSI Full Forecast [Titans_Invest]RSI Full Forecast

Get ready to experience the ultimate evolution of RSI-based indicators – the RSI Full Forecast, a boosted and even smarter version of the already powerful: RSI Forecast

Now featuring over 40 additional entry conditions (forecasts), this indicator redefines the way you view the market.

AI-Powered RSI Forecasting:

Using advanced linear regression with the least squares method – a solid foundation for machine learning - the RSI Full Forecast enables you to predict future RSI behavior with impressive accuracy.

But that’s not all: this new version also lets you monitor future crossovers between the RSI and the MA RSI, delivering early and strategic signals that go far beyond traditional analysis.

You’ll be able to monitor future crossovers up to 20 bars ahead, giving you an even broader and more precise view of market movements.

See the Future, Now:

• Track upcoming RSI & RSI MA crossovers in advance.

• Identify potential reversal zones before price reacts.

• Uncover statistical behavior patterns that would normally go unnoticed.

40+ Intelligent Conditions:

The new layer of conditions is designed to detect multiple high-probability scenarios based on historical patterns and predictive modeling. Each additional forecast is a window into the price's future, powered by robust mathematics and advanced algorithmic logic.

Full Customization:

All parameters can be tailored to fit your strategy – from smoothing periods to prediction sensitivity. You have complete control to turn raw data into smart decisions.

Innovative, Accurate, Unique:

This isn’t just an upgrade. It’s a quantum leap in technical analysis.

RSI Full Forecast is the first of its kind: an indicator that blends statistical analysis, machine learning, and visual design to create a true real-time predictive system.

⯁ SCIENTIFIC BASIS LINEAR REGRESSION

Linear Regression is a fundamental method of statistics and machine learning, used to model the relationship between a dependent variable y and one or more independent variables 𝑥.

The general formula for a simple linear regression is given by:

y = β₀ + β₁x + ε

β₁ = Σ((xᵢ - x̄)(yᵢ - ȳ)) / Σ((xᵢ - x̄)²)

β₀ = ȳ - β₁x̄

Where:

y = is the predicted variable (e.g. future value of RSI)

x = is the explanatory variable (e.g. time or bar index)

β0 = is the intercept (value of 𝑦 when 𝑥 = 0)

𝛽1 = is the slope of the line (rate of change)

ε = is the random error term

The goal is to estimate the coefficients 𝛽0 and 𝛽1 so as to minimize the sum of the squared errors — the so-called Random Error Method Least Squares.

⯁ LEAST SQUARES ESTIMATION

To minimize the error between predicted and observed values, we use the following formulas:

β₁ = /

β₀ = ȳ - β₁x̄

Where:

∑ = sum

x̄ = mean of x

ȳ = mean of y

x_i, y_i = individual values of the variables.

Where:

x_i and y_i are the means of the independent and dependent variables, respectively.

i ranges from 1 to n, the number of observations.

These equations guarantee the best linear unbiased estimator, according to the Gauss-Markov theorem, assuming homoscedasticity and linearity.

⯁ LINEAR REGRESSION IN MACHINE LEARNING

Linear regression is one of the cornerstones of supervised learning. Its simplicity and ability to generate accurate quantitative predictions make it essential in AI systems, predictive algorithms, time series analysis, and automated trading strategies.

By applying this model to the RSI, you are literally putting artificial intelligence at the heart of a classic indicator, bringing a new dimension to technical analysis.

⯁ VISUAL INTERPRETATION

Imagine an RSI time series like this:

Time →

RSI →

The regression line will smooth these values and extend them n periods into the future, creating a predicted trajectory based on the historical moment. This line becomes the predicted RSI, which can be crossed with the actual RSI to generate more intelligent signals.

⯁ SUMMARY OF SCIENTIFIC CONCEPTS USED

Linear Regression Models the relationship between variables using a straight line.

Least Squares Minimizes the sum of squared errors between prediction and reality.

Time Series Forecasting Estimates future values based on historical data.

Supervised Learning Trains models to predict outputs from known inputs.

Statistical Smoothing Reduces noise and reveals underlying trends.

⯁ WHY THIS INDICATOR IS REVOLUTIONARY

Scientifically-based: Based on statistical theory and mathematical inference.

Unprecedented: First public RSI with least squares predictive modeling.

Intelligent: Built with machine learning logic.

Practical: Generates forward-thinking signals.

Customizable: Flexible for any trading strategy.

⯁ CONCLUSION

By combining RSI with linear regression, this indicator allows a trader to predict market momentum, not just follow it.

RSI Full Forecast is not just an indicator — it is a scientific breakthrough in technical analysis technology.

⯁ Example of simple linear regression, which has one independent variable:

⯁ In linear regression, observations ( red ) are considered to be the result of random deviations ( green ) from an underlying relationship ( blue ) between a dependent variable ( y ) and an independent variable ( x ).

⯁ Visualizing heteroscedasticity in a scatterplot against 100 random fitted values using Matlab:

⯁ The data sets in the Anscombe's quartet are designed to have approximately the same linear regression line (as well as nearly identical means, standard deviations, and correlations) but are graphically very different. This illustrates the pitfalls of relying solely on a fitted model to understand the relationship between variables.

⯁ The result of fitting a set of data points with a quadratic function:

_________________________________________________

🔮 Linear Regression: PineScript Technical Parameters 🔮

_________________________________________________

Forecast Types:

• Flat: Assumes prices will remain the same.

• Linreg: Makes a 'Linear Regression' forecast for n periods.

Technical Information:

ta.linreg (built-in function)

Linear regression curve. A line that best fits the specified prices over a user-defined time period. It is calculated using the least squares method. The result of this function is calculated using the formula: linreg = intercept + slope * (length - 1 - offset), where intercept and slope are the values calculated using the least squares method on the source series.

Syntax:

• Function: ta.linreg()

Parameters:

• source: Source price series.

• length: Number of bars (period).

• offset: Offset.

• return: Linear regression curve.

This function has been cleverly applied to the RSI, making it capable of projecting future values based on past statistical trends.

______________________________________________________

______________________________________________________

⯁ WHAT IS THE RSI❓

The Relative Strength Index (RSI) is a technical analysis indicator developed by J. Welles Wilder. It measures the magnitude of recent price movements to evaluate overbought or oversold conditions in a market. The RSI is an oscillator that ranges from 0 to 100 and is commonly used to identify potential reversal points, as well as the strength of a trend.

⯁ HOW TO USE THE RSI❓

The RSI is calculated based on average gains and losses over a specified period (usually 14 periods). It is plotted on a scale from 0 to 100 and includes three main zones:

• Overbought: When the RSI is above 70, indicating that the asset may be overbought.

• Oversold: When the RSI is below 30, indicating that the asset may be oversold.

• Neutral Zone: Between 30 and 70, where there is no clear signal of overbought or oversold conditions.

______________________________________________________

______________________________________________________

⯁ ENTRY CONDITIONS

The conditions below are fully flexible and allow for complete customization of the signal.

______________________________________________________

______________________________________________________

🔹 CONDITIONS TO BUY 📈

______________________________________________________

• Signal Validity: The signal will remain valid for X bars .

• Signal Sequence: Configurable as AND or OR .

📈 RSI Conditions:

🔹 RSI > Upper

🔹 RSI < Upper

🔹 RSI > Lower

🔹 RSI < Lower

🔹 RSI > Middle

🔹 RSI < Middle

🔹 RSI > MA

🔹 RSI < MA

📈 MA Conditions:

🔹 MA > Upper

🔹 MA < Upper

🔹 MA > Lower

🔹 MA < Lower

📈 Crossovers:

🔹 RSI (Crossover) Upper

🔹 RSI (Crossunder) Upper

🔹 RSI (Crossover) Lower

🔹 RSI (Crossunder) Lower

🔹 RSI (Crossover) Middle

🔹 RSI (Crossunder) Middle

🔹 RSI (Crossover) MA

🔹 RSI (Crossunder) MA

🔹 MA (Crossover) Upper

🔹 MA (Crossunder) Upper

🔹 MA (Crossover) Lower

🔹 MA (Crossunder) Lower

📈 RSI Divergences:

🔹 RSI Divergence Bull

🔹 RSI Divergence Bear

📈 RSI Forecast:

🔹 RSI (Crossover) MA Forecast

🔹 RSI (Crossunder) MA Forecast

🔹 RSI Forecast 1 > MA Forecast 1

🔹 RSI Forecast 1 < MA Forecast 1

🔹 RSI Forecast 2 > MA Forecast 2

🔹 RSI Forecast 2 < MA Forecast 2

🔹 RSI Forecast 3 > MA Forecast 3

🔹 RSI Forecast 3 < MA Forecast 3

🔹 RSI Forecast 4 > MA Forecast 4

🔹 RSI Forecast 4 < MA Forecast 4

🔹 RSI Forecast 5 > MA Forecast 5

🔹 RSI Forecast 5 < MA Forecast 5

🔹 RSI Forecast 6 > MA Forecast 6

🔹 RSI Forecast 6 < MA Forecast 6

🔹 RSI Forecast 7 > MA Forecast 7

🔹 RSI Forecast 7 < MA Forecast 7

🔹 RSI Forecast 8 > MA Forecast 8

🔹 RSI Forecast 8 < MA Forecast 8

🔹 RSI Forecast 9 > MA Forecast 9

🔹 RSI Forecast 9 < MA Forecast 9

🔹 RSI Forecast 10 > MA Forecast 10

🔹 RSI Forecast 10 < MA Forecast 10

🔹 RSI Forecast 11 > MA Forecast 11

🔹 RSI Forecast 11 < MA Forecast 11

🔹 RSI Forecast 12 > MA Forecast 12

🔹 RSI Forecast 12 < MA Forecast 12

🔹 RSI Forecast 13 > MA Forecast 13

🔹 RSI Forecast 13 < MA Forecast 13

🔹 RSI Forecast 14 > MA Forecast 14

🔹 RSI Forecast 14 < MA Forecast 14

🔹 RSI Forecast 15 > MA Forecast 15

🔹 RSI Forecast 15 < MA Forecast 15

🔹 RSI Forecast 16 > MA Forecast 16

🔹 RSI Forecast 16 < MA Forecast 16

🔹 RSI Forecast 17 > MA Forecast 17

🔹 RSI Forecast 17 < MA Forecast 17

🔹 RSI Forecast 18 > MA Forecast 18

🔹 RSI Forecast 18 < MA Forecast 18

🔹 RSI Forecast 19 > MA Forecast 19

🔹 RSI Forecast 19 < MA Forecast 19

🔹 RSI Forecast 20 > MA Forecast 20

🔹 RSI Forecast 20 < MA Forecast 20

______________________________________________________

______________________________________________________

🔸 CONDITIONS TO SELL 📉

______________________________________________________

• Signal Validity: The signal will remain valid for X bars .

• Signal Sequence: Configurable as AND or OR .

📉 RSI Conditions:

🔸 RSI > Upper

🔸 RSI < Upper

🔸 RSI > Lower

🔸 RSI < Lower

🔸 RSI > Middle

🔸 RSI < Middle

🔸 RSI > MA

🔸 RSI < MA

📉 MA Conditions:

🔸 MA > Upper

🔸 MA < Upper

🔸 MA > Lower

🔸 MA < Lower

📉 Crossovers:

🔸 RSI (Crossover) Upper

🔸 RSI (Crossunder) Upper

🔸 RSI (Crossover) Lower

🔸 RSI (Crossunder) Lower

🔸 RSI (Crossover) Middle

🔸 RSI (Crossunder) Middle

🔸 RSI (Crossover) MA

🔸 RSI (Crossunder) MA

🔸 MA (Crossover) Upper

🔸 MA (Crossunder) Upper

🔸 MA (Crossover) Lower

🔸 MA (Crossunder) Lower

📉 RSI Divergences:

🔸 RSI Divergence Bull

🔸 RSI Divergence Bear

📉 RSI Forecast:

🔸 RSI (Crossover) MA Forecast

🔸 RSI (Crossunder) MA Forecast

🔸 RSI Forecast 1 > MA Forecast 1

🔸 RSI Forecast 1 < MA Forecast 1

🔸 RSI Forecast 2 > MA Forecast 2

🔸 RSI Forecast 2 < MA Forecast 2

🔸 RSI Forecast 3 > MA Forecast 3

🔸 RSI Forecast 3 < MA Forecast 3

🔸 RSI Forecast 4 > MA Forecast 4

🔸 RSI Forecast 4 < MA Forecast 4

🔸 RSI Forecast 5 > MA Forecast 5

🔸 RSI Forecast 5 < MA Forecast 5

🔸 RSI Forecast 6 > MA Forecast 6

🔸 RSI Forecast 6 < MA Forecast 6

🔸 RSI Forecast 7 > MA Forecast 7

🔸 RSI Forecast 7 < MA Forecast 7

🔸 RSI Forecast 8 > MA Forecast 8

🔸 RSI Forecast 8 < MA Forecast 8

🔸 RSI Forecast 9 > MA Forecast 9

🔸 RSI Forecast 9 < MA Forecast 9

🔸 RSI Forecast 10 > MA Forecast 10

🔸 RSI Forecast 10 < MA Forecast 10

🔸 RSI Forecast 11 > MA Forecast 11

🔸 RSI Forecast 11 < MA Forecast 11

🔸 RSI Forecast 12 > MA Forecast 12

🔸 RSI Forecast 12 < MA Forecast 12

🔸 RSI Forecast 13 > MA Forecast 13

🔸 RSI Forecast 13 < MA Forecast 13

🔸 RSI Forecast 14 > MA Forecast 14

🔸 RSI Forecast 14 < MA Forecast 14

🔸 RSI Forecast 15 > MA Forecast 15

🔸 RSI Forecast 15 < MA Forecast 15

🔸 RSI Forecast 16 > MA Forecast 16

🔸 RSI Forecast 16 < MA Forecast 16

🔸 RSI Forecast 17 > MA Forecast 17

🔸 RSI Forecast 17 < MA Forecast 17

🔸 RSI Forecast 18 > MA Forecast 18

🔸 RSI Forecast 18 < MA Forecast 18

🔸 RSI Forecast 19 > MA Forecast 19

🔸 RSI Forecast 19 < MA Forecast 19

🔸 RSI Forecast 20 > MA Forecast 20

🔸 RSI Forecast 20 < MA Forecast 20

______________________________________________________

______________________________________________________

🤖 AUTOMATION 🤖

• You can automate the BUY and SELL signals of this indicator.

______________________________________________________

______________________________________________________

⯁ UNIQUE FEATURES

______________________________________________________

Linear Regression: (Forecast)

Signal Validity: The signal will remain valid for X bars

Signal Sequence: Configurable as AND/OR

Condition Table: BUY/SELL

Condition Labels: BUY/SELL

Plot Labels in the Graph Above: BUY/SELL

Automate and Monitor Signals/Alerts: BUY/SELL

Linear Regression (Forecast)

Signal Validity: The signal will remain valid for X bars

Signal Sequence: Configurable as AND/OR

Condition Table: BUY/SELL

Condition Labels: BUY/SELL

Plot Labels in the Graph Above: BUY/SELL

Automate and Monitor Signals/Alerts: BUY/SELL

______________________________________________________

📜 SCRIPT : RSI Full Forecast

🎴 Art by : @Titans_Invest & @DiFlip

👨💻 Dev by : @Titans_Invest & @DiFlip

🎑 Titans Invest — The Wizards Without Gloves 🧤

✨ Enjoy!

______________________________________________________

o Mission 🗺

• Inspire Traders to manifest Magic in the Market.

o Vision 𐓏

• To elevate collective Energy 𐓷𐓏

RSI Forecast [Titans_Invest]RSI Forecast

Introducing one of the most impressive RSI indicators ever created – arguably the best on TradingView, and potentially the best in the world.

RSI Forecast is a visionary evolution of the classic RSI, merging powerful customization with groundbreaking predictive capabilities. While preserving the core principles of traditional RSI, it takes analysis to the next level by allowing users to anticipate potential future RSI movements.

Real-Time RSI Forecasting:

For the first time ever, an RSI indicator integrates linear regression using the least squares method to accurately forecast the future behavior of the RSI. This innovation empowers traders to stay one step ahead of the market with forward-looking insight.

Highly Customizable:

Easily adapt the indicator to your personal trading style. Fine-tune a variety of parameters to generate signals perfectly aligned with your strategy.

Innovative, Unique, and Powerful:

This is the world’s first RSI Forecast to apply this predictive approach using least squares linear regression. A truly elite-level tool designed for traders who want a real edge in the market.

⯁ SCIENTIFIC BASIS LINEAR REGRESSION

Linear Regression is a fundamental method of statistics and machine learning, used to model the relationship between a dependent variable y and one or more independent variables 𝑥.

The general formula for a simple linear regression is given by:

y = β₀ + β₁x + ε

Where:

y = is the predicted variable (e.g. future value of RSI)

x = is the explanatory variable (e.g. time or bar index)

β0 = is the intercept (value of 𝑦 when 𝑥 = 0)

𝛽1 = is the slope of the line (rate of change)

ε = is the random error term

The goal is to estimate the coefficients 𝛽0 and 𝛽1 so as to minimize the sum of the squared errors — the so-called Random Error Method Least Squares.

⯁ LEAST SQUARES ESTIMATION

To minimize the error between predicted and observed values, we use the following formulas:

β₁ = /

β₀ = ȳ - β₁x̄

Where:

∑ = sum

x̄ = mean of x

ȳ = mean of y

x_i, y_i = individual values of the variables.

Where:

x_i and y_i are the means of the independent and dependent variables, respectively.

i ranges from 1 to n, the number of observations.

These equations guarantee the best linear unbiased estimator, according to the Gauss-Markov theorem, assuming homoscedasticity and linearity.

⯁ LINEAR REGRESSION IN MACHINE LEARNING

Linear regression is one of the cornerstones of supervised learning. Its simplicity and ability to generate accurate quantitative predictions make it essential in AI systems, predictive algorithms, time series analysis, and automated trading strategies.

By applying this model to the RSI, you are literally putting artificial intelligence at the heart of a classic indicator, bringing a new dimension to technical analysis.

⯁ VISUAL INTERPRETATION

Imagine an RSI time series like this:

Time →

RSI →

The regression line will smooth these values and extend them n periods into the future, creating a predicted trajectory based on the historical moment. This line becomes the predicted RSI, which can be crossed with the actual RSI to generate more intelligent signals.

⯁ SUMMARY OF SCIENTIFIC CONCEPTS USED

Linear Regression Models the relationship between variables using a straight line.

Least Squares Minimizes the sum of squared errors between prediction and reality.

Time Series Forecasting Estimates future values based on historical data.

Supervised Learning Trains models to predict outputs from known inputs.

Statistical Smoothing Reduces noise and reveals underlying trends.

⯁ WHY THIS INDICATOR IS REVOLUTIONARY

Scientifically-based: Based on statistical theory and mathematical inference.

Unprecedented: First public RSI with least squares predictive modeling.

Intelligent: Built with machine learning logic.

Practical: Generates forward-thinking signals.

Customizable: Flexible for any trading strategy.

⯁ CONCLUSION

By combining RSI with linear regression, this indicator allows a trader to predict market momentum, not just follow it.

RSI Forecast is not just an indicator — it is a scientific breakthrough in technical analysis technology.

⯁ Example of simple linear regression, which has one independent variable:

⯁ In linear regression, observations ( red ) are considered to be the result of random deviations ( green ) from an underlying relationship ( blue ) between a dependent variable ( y ) and an independent variable ( x ).

⯁ Visualizing heteroscedasticity in a scatterplot against 100 random fitted values using Matlab:

⯁ The data sets in the Anscombe's quartet are designed to have approximately the same linear regression line (as well as nearly identical means, standard deviations, and correlations) but are graphically very different. This illustrates the pitfalls of relying solely on a fitted model to understand the relationship between variables.

⯁ The result of fitting a set of data points with a quadratic function:

_______________________________________________________________________

🥇 This is the world’s first RSI indicator with: Linear Regression for Forecasting 🥇_______________________________________________________________________

_________________________________________________

🔮 Linear Regression: PineScript Technical Parameters 🔮

_________________________________________________

Forecast Types:

• Flat: Assumes prices will remain the same.

• Linreg: Makes a 'Linear Regression' forecast for n periods.

Technical Information:

ta.linreg (built-in function)

Linear regression curve. A line that best fits the specified prices over a user-defined time period. It is calculated using the least squares method. The result of this function is calculated using the formula: linreg = intercept + slope * (length - 1 - offset), where intercept and slope are the values calculated using the least squares method on the source series.

Syntax:

• Function: ta.linreg()

Parameters:

• source: Source price series.

• length: Number of bars (period).

• offset: Offset.

• return: Linear regression curve.

This function has been cleverly applied to the RSI, making it capable of projecting future values based on past statistical trends.

______________________________________________________

______________________________________________________

⯁ WHAT IS THE RSI❓

The Relative Strength Index (RSI) is a technical analysis indicator developed by J. Welles Wilder. It measures the magnitude of recent price movements to evaluate overbought or oversold conditions in a market. The RSI is an oscillator that ranges from 0 to 100 and is commonly used to identify potential reversal points, as well as the strength of a trend.

⯁ HOW TO USE THE RSI❓

The RSI is calculated based on average gains and losses over a specified period (usually 14 periods). It is plotted on a scale from 0 to 100 and includes three main zones:

• Overbought: When the RSI is above 70, indicating that the asset may be overbought.

• Oversold: When the RSI is below 30, indicating that the asset may be oversold.

• Neutral Zone: Between 30 and 70, where there is no clear signal of overbought or oversold conditions.

______________________________________________________

______________________________________________________

⯁ ENTRY CONDITIONS

The conditions below are fully flexible and allow for complete customization of the signal.

______________________________________________________

______________________________________________________

🔹 CONDITIONS TO BUY 📈

______________________________________________________

• Signal Validity: The signal will remain valid for X bars .

• Signal Sequence: Configurable as AND or OR .

📈 RSI Conditions:

🔹 RSI > Upper

🔹 RSI < Upper

🔹 RSI > Lower

🔹 RSI < Lower

🔹 RSI > Middle

🔹 RSI < Middle

🔹 RSI > MA

🔹 RSI < MA

📈 MA Conditions:

🔹 MA > Upper

🔹 MA < Upper

🔹 MA > Lower

🔹 MA < Lower

📈 Crossovers:

🔹 RSI (Crossover) Upper

🔹 RSI (Crossunder) Upper

🔹 RSI (Crossover) Lower

🔹 RSI (Crossunder) Lower

🔹 RSI (Crossover) Middle

🔹 RSI (Crossunder) Middle

🔹 RSI (Crossover) MA

🔹 RSI (Crossunder) MA

🔹 MA (Crossover) Upper

🔹 MA (Crossunder) Upper

🔹 MA (Crossover) Lower

🔹 MA (Crossunder) Lower

📈 RSI Divergences:

🔹 RSI Divergence Bull

🔹 RSI Divergence Bear

📈 RSI Forecast:

🔮 RSI (Crossover) MA Forecast

🔮 RSI (Crossunder) MA Forecast

______________________________________________________

______________________________________________________

🔸 CONDITIONS TO SELL 📉

______________________________________________________

• Signal Validity: The signal will remain valid for X bars .

• Signal Sequence: Configurable as AND or OR .

📉 RSI Conditions:

🔸 RSI > Upper

🔸 RSI < Upper

🔸 RSI > Lower

🔸 RSI < Lower

🔸 RSI > Middle

🔸 RSI < Middle

🔸 RSI > MA

🔸 RSI < MA

📉 MA Conditions:

🔸 MA > Upper

🔸 MA < Upper

🔸 MA > Lower

🔸 MA < Lower

📉 Crossovers:

🔸 RSI (Crossover) Upper

🔸 RSI (Crossunder) Upper

🔸 RSI (Crossover) Lower

🔸 RSI (Crossunder) Lower

🔸 RSI (Crossover) Middle

🔸 RSI (Crossunder) Middle

🔸 RSI (Crossover) MA

🔸 RSI (Crossunder) MA

🔸 MA (Crossover) Upper

🔸 MA (Crossunder) Upper

🔸 MA (Crossover) Lower

🔸 MA (Crossunder) Lower

📉 RSI Divergences:

🔸 RSI Divergence Bull

🔸 RSI Divergence Bear

📉 RSI Forecast:

🔮 RSI (Crossover) MA Forecast

🔮 RSI (Crossunder) MA Forecast

______________________________________________________

______________________________________________________

🤖 AUTOMATION 🤖

• You can automate the BUY and SELL signals of this indicator.

______________________________________________________

______________________________________________________

⯁ UNIQUE FEATURES

______________________________________________________

Linear Regression: (Forecast)

Signal Validity: The signal will remain valid for X bars

Signal Sequence: Configurable as AND/OR

Condition Table: BUY/SELL

Condition Labels: BUY/SELL

Plot Labels in the Graph Above: BUY/SELL

Automate and Monitor Signals/Alerts: BUY/SELL

Linear Regression (Forecast)

Signal Validity: The signal will remain valid for X bars

Signal Sequence: Configurable as AND/OR

Condition Table: BUY/SELL

Condition Labels: BUY/SELL

Plot Labels in the Graph Above: BUY/SELL

Automate and Monitor Signals/Alerts: BUY/SELL

______________________________________________________

📜 SCRIPT : RSI Forecast

🎴 Art by : @Titans_Invest & @DiFlip

👨💻 Dev by : @Titans_Invest & @DiFlip

🎑 Titans Invest — The Wizards Without Gloves 🧤

✨ Enjoy!

______________________________________________________

o Mission 🗺

• Inspire Traders to manifest Magic in the Market.

o Vision 𐓏

• To elevate collective Energy 𐓷𐓏

RSI Full [Titans_Invest]RSI Full

One of the most complete RSI indicators on the market.

While maintaining the classic RSI foundation, our indicator integrates multiple entry conditions to generate more accurate buy and sell signals.

All conditions are fully configurable, allowing complete customization to fit your trading strategy.

⯁ WHAT IS THE RSI❓

The Relative Strength Index (RSI) is a technical analysis indicator developed by J. Welles Wilder. It measures the magnitude of recent price movements to evaluate overbought or oversold conditions in a market. The RSI is an oscillator that ranges from 0 to 100 and is commonly used to identify potential reversal points, as well as the strength of a trend.

⯁ HOW TO USE THE RSI❓

The RSI is calculated based on average gains and losses over a specified period (usually 14 periods). It is plotted on a scale from 0 to 100 and includes three main zones:

Overbought: When the RSI is above 70, indicating that the asset may be overbought.

Oversold: When the RSI is below 30, indicating that the asset may be oversold.

Neutral Zone: Between 30 and 70, where there is no clear signal of overbought or oversold conditions.

⯁ ENTRY CONDITIONS

The conditions below are fully flexible and allow for complete customization of the signal.

______________________________________________________

🔹 CONDITIONS TO BUY 📈

______________________________________________________

• Signal Validity: The signal will remain valid for X bars .

• Signal Sequence: Configurable as AND/OR .

📈 RSI Conditions:

🔹 RSI > Upper

🔹 RSI < Upper

🔹 RSI > Lower

🔹 RSI < Lower

🔹 RSI > Middle

🔹 RSI < Middle

🔹 RSI > MA

🔹 RSI < MA

📈 MA Conditions:

🔹 MA > Upper

🔹 MA < Upper

🔹 MA > Lower

🔹 MA < Lower

📈 Crossovers:

🔹 RSI (Crossover) Upper

🔹 RSI (Crossunder) Upper

🔹 RSI (Crossover) Lower

🔹 RSI (Crossunder) Lower

🔹 RSI (Crossover) Middle

🔹 RSI (Crossunder) Middle

🔹 RSI (Crossover) MA

🔹 RSI (Crossunder) MA

🔹 MA (Crossover) Upper

🔹 MA (Crossunder) Upper

🔹 MA (Crossover) Lower

🔹 MA (Crossunder) Lower

📈 RSI Divergences:

🔹 RSI Divergence Bull

🔹 RSI Divergence Bear

______________________________________________________

______________________________________________________

🔸 CONDITIONS TO SELL 📉

______________________________________________________

• Signal Validity: The signal will remain valid for X bars .

• Signal Sequence: Configurable as AND/OR .

📉 RSI Conditions:

🔸 RSI > Upper

🔸 RSI < Upper

🔸 RSI > Lower

🔸 RSI < Lower

🔸 RSI > Middle

🔸 RSI < Middle

🔸 RSI > MA

🔸 RSI < MA

📉 MA Conditions:

🔸 MA > Upper

🔸 MA < Upper

🔸 MA > Lower

🔸 MA < Lower

📉 Crossovers:

🔸 RSI (Crossover) Upper

🔸 RSI (Crossunder) Upper

🔸 RSI (Crossover) Lower

🔸 RSI (Crossunder) Lower

🔸 RSI (Crossover) Middle

🔸 RSI (Crossunder) Middle

🔸 RSI (Crossover) MA

🔸 RSI (Crossunder) MA

🔸 MA (Crossover) Upper

🔸 MA (Crossunder) Upper

🔸 MA (Crossover) Lower

🔸 MA (Crossunder) Lower

📉 RSI Divergences:

🔸 RSI Divergence Bull

🔸 RSI Divergence Bear

______________________________________________________

______________________________________________________

🤖 AUTOMATION 🤖

• You can automate the BUY and SELL signals of this indicator.

______________________________________________________

______________________________________________________

⯁ UNIQUE FEATURES

______________________________________________________

Signal Validity: The signal will remain valid for X bars

Signal Sequence: Configurable as AND/OR

Condition Table: BUY/SELL

Condition Labels: BUY/SELL

Plot Labels in the Graph Above: BUY/SELL

Automate and Monitor Signals/Alerts: BUY/SELL

Signal Validity: The signal will remain valid for X bars

Signal Sequence: Configurable as AND/OR

Condition Table: BUY/SELL

Condition Labels: BUY/SELL

Plot Labels in the Graph Above: BUY/SELL

Automate and Monitor Signals/Alerts: BUY/SELL

______________________________________________________

📜 SCRIPT : RSI Full

🎴 Art by : @Titans_Invest & @DiFlip

👨💻 Dev by : @Titans_Invest & @DiFlip

🎑 Titans Invest — The Wizards Without Gloves 🧤

✨ Enjoy the Spell!

______________________________________________________

o Mission 🗺

• Inspire Traders to manifest Magic in the Market.

o Vision 𐓏

• To elevate collective Energy 𐓷𐓏

Statistical OHLC Projections [neo|]█ OVERVIEW

Statistical OHLC Projections is an indicator designed to offer users a customizable deep-dive on measuring historical price levels for any timeframe. The indicator separates price into two distinct levels, "Manipulation" and "Distribution", where the idea is that for higher timeframe candles, e.g. an up-close candle, the distance from the open to the bottom of the wick would constitute the Manipulation, and the rest would be considered the Distribution. By measuring out these levels, we can gain insight on how far the market may move from higher timeframe opens to their manipulations and distributions, and apply this knowledge to our analysis.

IMPORTANT: Since levels are based on the lookback available on your chart, if the levels aren't being displayed this likely means you don't have enough lookback for your selected timeframe. To check this, enable the stat table to see how many values are available for your timeframe, and either reduce the lookback or increase your chart timeframe.

█ CONCEPTS

The core concept revolves around understanding market behavior through the lens of historical candle structure. The indicator dissects OHLC data to provide statistical boundaries of expected price movement.

- Manipulation Levels: These represent the areas typically seen as liquidity grabs or false moves where price extends in one direction before reversing.

- Distribution Levels: These highlight where the bulk of directional movement tends to occur, often following the manipulation move.

The tool aggregates this data across your selected timeframe to inform you of potential levels associated with it.

█ FEATURES

Multiple Display Types: Display statistical data through two sleek styles, areas or lines. Where areas represent the area between two customizable lookback values, and lines represent one average value.

Adjustable Timeframe Selection: Whether you want to see data based on the 1D chart, or the 1W chart, anything is possible. Simply change the timeframe on the dropdown menu and if there is sufficient lookback the indicator will adjust to your requested timeframe.

Customizable Historical Lookback: By default, the indicator will measure the average 60 values of your requested timeframe, however this may be adjusted to be higher or lower based on your preference. If you want to measure recent moves, 10-20 lookback may be better for you, or if you want more data for less volatile instruments, a value of 100 may be better.

Historical Display: Prevent historical levels from being removed by unchecking the "Remove Previous Drawings" option, this will allow you to examine how the levels previously interacted with price.

NY Midnight Anchoring: By checking the "Use NY Midnight" option, you may see the projection anchored to the New York midnight open time, which is often a significant level on indices.

Alerts: You may enable alerts for any of the indicator's provided levels to stay informed, even when off the charts.

█ How to use

To use the indicator, simply apply it to your chart and modify any of your desired inputs.

By default, the indicator will provide levels for the "1D" timeframe, with a desired lookback of 60, on most instruments and plans this can be gotten when you are on the 30 minute timeframe or above.

When price reaches or extends beyond a manipulation level, observe how it reacts and whether it rejects from that level, if it does this may be an indication that the candle for the timeframe you selected may be reversing.

█ SETTINGS AND OPTIONS

Customize the indicator’s behavior, timeframe sources, and visual appearance to fit your analysis style. Each setting has been designed with flexibility in mind, whether you're working on lower or higher timeframes.

Display Mode: Switch between different display styles for levels: - Default: Shows all statistical levels as individual lines.

- Areas: Plots filled zones between two customizable lookbacks to represent the range between them.

This is ideal for visually mapping high-probability zones of price activity.

Timeframe Settings:

- Show First/Second Timeframe: Choose to show one or both timeframe projections simultaneously.

- First Timeframe / Second Timeframe: Define the higher timeframe candle you want to base calculations on (e.g., 1D, 1W).

- Use NY Midnight: When enabled and using the daily timeframe, the levels will be anchored to the New York Midnight Open (00:00 EST), a key institutional timing reference, especially useful for indices and forex.

Calculation Settings:

- Main Lookback Period: The number of historical candles used in the statistical calculations. A lower number focuses on recent price action, while a higher number smooths results across broader history.

- First Lookback / Second Lookback: Used when “Areas” mode is selected to define the range of the shaded zone. For example, an area from 20 to 60 candles creates a band between short- and long-term price behavior averages.

Visual Settings:

- Line Style: Set your preferred visual style: Solid, Dashed, or Dotted.

- Remove Previous Drawings: When enabled, only the most recent projection is shown on the chart. Disable to retain previous levels and visually backtest their reactions over time.

Color Settings:

Customize each level independently to match your chart theme:

- Manipulation High/Low

- Distribution High/Low

- Open Level

- Label Text Color

Premium/Discount Zones:

- Enable Premium/Discount Zones: Overlay price zones above and below equilibrium to visualize potential overbought (premium) and oversold (discount) areas.

- Premium/Discount Colors: Fully customizable zone colors for clarity and emphasis.

Table Settings:

- Show Statistics Table: Adds an on-chart table summarizing key levels from your active timeframe(s).

- Table Cell Color: Set the background color of the table cells for visibility.

- Table Position: Choose from preset chart locations to position the table where it works best for your layout.

Alerts:

Stay on top of price interactions with key levels even when you're away from the charts.

- Manipulation Hits (High)

- Manipulation Hits (Low)

- Distribution Hits (High)

- Distribution Hits (Low)

Combined EMA Technical AnalysisThis script is written in Pine Script (version 5) for TradingView and creates a comprehensive technical analysis indicator called "Combined EMA Technical Analysis." It overlays multiple technical indicators on a price chart, including Exponential Moving Averages (EMAs), VWAP, MACD, PSAR, RSI, Bollinger Bands, ADX, and external data from the S&P 500 (SPX) and VIX indices. The script also provides visual cues through colors, shapes, and a customizable table to help traders interpret market conditions.

Here’s a breakdown of the script:

---

### **1. Purpose**

- The script combines several popular technical indicators to analyze price trends, momentum, volatility, and market sentiment.

- It uses color coding (green for bullish, red for bearish, gray/white for neutral) and a table to display key information.

---

### **2. Custom Colors**

- Defines custom RGB colors for bullish (`customGreen`), bearish (`customRed`), and neutral (`neutralGray`) signals to enhance visual clarity.

---

### **3. User Inputs**

- **EMA Colors**: Users can customize the colors of five EMAs (8, 20, 9, 21, 50 periods).

- **MACD Settings**: Adjustable short length (12), long length (26), and signal length (9).

- **RSI Settings**: Adjustable length (14).

- **Bollinger Bands Settings**: Length (20), multiplier (2), and proximity threshold (0.1% of band width).

- **ADX Settings**: Adjustable length (14).

- **Table Settings**: Position (e.g., "Bottom Right") and text size (e.g., "Small").

---

### **4. Indicator Calculations**

#### **Exponential Moving Averages (EMAs)**

- Calculates five EMAs: 8, 20, 9, 21, and 50 periods based on the closing price.

- Used to identify short-term and long-term trends.

#### **Volume Weighted Average Price (VWAP)**

- Resets daily and calculates the average price weighted by volume.

- Color-coded: green if price > VWAP (bullish), red if price < VWAP (bearish), white if neutral.

#### **MACD (Moving Average Convergence Divergence)**

- Uses short (12) and long (26) EMAs to compute the MACD line, with a 9-period signal line.

- Displays "Bullish" (green) if MACD > signal, "Bearish" (red) if MACD < signal.

#### **Parabolic SAR (PSAR)**

- Calculated with acceleration factors (start: 0.02, increment: 0.02, max: 0.2).

- Indicates trend direction: green if price > PSAR (bullish), red if price < PSAR (bearish).

#### **Relative Strength Index (RSI)**

- Measures momentum over 14 periods.

- Highlighted in green if > 70 (overbought), red if < 30 (oversold), white otherwise.

#### **Bollinger Bands (BB)**

- Uses a 20-period SMA with a 2-standard-deviation multiplier.

- Color-coded based on price position:

- Green: Above upper band or close to it.

- Red: Below lower band or close to it.

- Gray: Neutral (within bands).

#### **Average Directional Index (ADX)**

- Manually calculates ADX to measure trend strength:

- Strong trend: ADX > 25.

- Very strong trend: ADX > 50.

- Direction: Bullish if +DI > -DI, bearish if -DI > +DI.

#### **EMA Crosses**

- Detects bullish (crossover) and bearish (crossunder) events for:

- EMA 9 vs. EMA 21.

- EMA 8 vs. EMA 20.

- Visualized with green (bullish) or red (bearish) circles.

#### **SPX and VIX Data**

- Fetches daily closing prices for the S&P 500 (SPX) and VIX (volatility index).

- SPX trend: Bullish if EMA 9 > EMA 21, bearish if EMA 9 < EMA 21.

- VIX levels: High (> 25, fear), Low (< 15, stability).

- VIX color: Green if SPX bullish and VIX low, red if SPX bearish and VIX high, white otherwise.

---

### **5. Visual Outputs**

#### **Plots**

- EMAs, VWAP, and PSAR are plotted on the chart with their respective colors.

- EMA crosses are marked with circles (green for bullish, red for bearish).

#### **Table**

- Displays a summary of indicators in a customizable position and size.

- Indicators shown (if enabled):

- EMA 8/20, 9/21, 50: Green dot if bullish, red if bearish.

- VWAP: Green if price > VWAP, red if price < VWAP.

- MACD: Green if bullish, red if bearish.

- MACD Zero: Green if MACD > 0, red if MACD < 0.

- PSAR: Green if price > PSAR, red if price < PSAR.

- ADX: Arrows for very strong trends (↑/↓), dots for weaker trends, colored by direction.

- Bollinger Bands: Arrows (↑/↓) or dots based on price position.

- RSI: Numeric value, colored by overbought/oversold levels.

- VIX: Numeric value, colored based on SPX trend and VIX level.

---

### **6. Alerts**

- Triggers alerts for EMA 8/20 crosses:

- Bullish: "EMA 8/20 Bullish Cross on Candle Close!"

- Bearish: "EMA 8/20 Bearish Cross on Candle Close!"

---

### **7. Key Features**

- **Flexibility**: Users can toggle indicators on/off in the table and adjust parameters.

- **Visual Clarity**: Consistent use of green (bullish), red (bearish), and neutral colors.

- **Comprehensive**: Combines trend, momentum, volatility, and market sentiment indicators.

---

### **How to Use**

1. Add the script to TradingView.

2. Customize inputs (colors, lengths, table position) as needed.

3. Interpret the chart and table:

- Green signals suggest bullish conditions.

- Red signals suggest bearish conditions.

- Neutral signals indicate indecision or consolidation.

4. Set up alerts for EMA crosses to catch trend changes.

This script is ideal for traders who want a multi-indicator dashboard to monitor price action and market conditions efficiently.

Uptrick Signal Density Cloud🟪 Introduction

The Uptrick Signal Density Cloud is designed to track market direction and highlight potential reversals or shifts in momentum. It plots two smoothed lines on the chart and fills the space between them (often called a “cloud”). The bars on the chart change color depending on bullish or bearish conditions, and small triangles appear when certain reversal criteria are met. A metrics table displays real-time values for easy reference.

🟩 Why These Features Have Been Linked Together

1) Dual-Line Structure

Two separate lines represent shorter- and longer-term market tendencies. Linking them in one tool allows traders to view both near-term changes and the broader directional bias in a single glance.

2) Smoothed Averages

The script offers multiple smoothing methods—exponential, simple, hull, and an optimized approach—to reduce noise. Using more than one type of moving average can help balance responsiveness with stability.

3) Density Cloud Concept

Shading the region between the two lines highlights the gap or “thickness.” A wider gap typically signals stronger momentum, while a narrower gap could indicate a weakening trend or potential market indecision. When the cloud is too wide and crosses a certain threshold defined by the user, it indicates a possible reversal. When the cloud is too narrow it may indicate a potential breakout.

🟪 Why Use This Indicator

• Trend Visibility: The color-coded lines and bars make it easier to distinguish bullish from bearish conditions.

• Momentum Tracking: Thicker cloud regions suggest stronger separation between the faster and slower lines, potentially indicating robust momentum.

• Possible Reversal Alerts: Small triangles appear within thick zones when the indicator detects a crossover, drawing attention to key moments of potential trend change.

• Quick Reference Table: A metrics table shows line values, bullish or bearish status, and cloud thickness without needing to hover over chart elements.

🟩 Inputs

1) First Smoothing Length (length1)

Default: 14

Defines the lookback period for the faster line. Lower values make the line respond more quickly to price changes.

2) Second Smoothing Length (length2)

Default: 28

Defines the lookback period for the slower line or one of the moving averages in optimized mode. It generally responds more slowly than the faster line.

3) Extra Smoothing Length (extraLength)

Default: 50

A medium-term period commonly seen in technical analysis. In optimized mode, it helps add broader perspective to the combined lines.

4) Source (source)

Default: close

Specifies the price data (for example, open, high, low, or a custom source) used in the calculations.

5) Cloud Type (cloudType)

Options: Optimized, EMA, SMA, HMA

Determines the smoothing method used for the lines. “Optimized” blends multiple exponential averages at different lengths.

6) Cloud Thickness Threshold (thicknessThreshold)

Default: 0.5

Sets the minimum separation between the two lines to qualify as a “thick” zone, indicating potentially stronger momentum.

🟪 Core Components

1) Faster and Slower Lines

Each line is smoothed according to user preferences or the optimized technique. The faster line typically reacts more quickly, while the slower line provides a broader overview.

2) Filled Density Cloud

The space between the two lines is filled to visualize in which direction the market is trending.

3) Color-Coded Bars

Price bars adopt bullish or bearish colors based on which line is on top, providing an immediate sense of trend direction.

4) Reversal Triangles

When the cloud is thick (exceeding the threshold) and the lines cross in the opposite direction, small triangles appear, signaling a possible market shift.

5) Metrics Table

A compact table shows the current values of both lines, their bullish/bearish statuses, the cloud thickness, and whether the cloud is in a “reversal zone.”

🟩 Calculation Process

1) Raw Averages

Depending on the mode, standard exponential, simple, hull, or “optimized” exponential blends are calculated.

2) Optimized Averages (if selected)

The faster line is the average of three exponential moving averages using length1, length2, and extraLength.

The slower line similarly uses those same lengths multiplied by 1.5, then averages them together for broader smoothing.

3) Difference and Threshold

The absolute gap between the two lines is measured. When it exceeds thicknessThreshold, the cloud is considered thick.

4) Bullish or Bearish Determination

If sma1 (the faster line) is above sma2 (the slower line), conditions are deemed bullish; otherwise, they are bearish. This distinction is reflected in both bar colors and cloud shading.

5) Reversal Markers

In thick zones, a crossover triggers a triangle at the point of potential reversal, alerting traders to a possible trend change.

🟪 Smoothing Methods

1) Exponential (EMA)

Prioritizes recent data for quicker responsiveness.

2) Simple (SMA)

Takes a straightforward average of the chosen period, smoothing price action but often lagging more in volatile markets.

3) Hull (HMA)

Employs a specialized formula to reduce lag while maintaining smoothness.

4) Optimized (Blended Exponential)

Combines multiple EMA calculations to strike a balance between responsiveness and noise reduction.

🟩 Cloud Logic and Reversal Zones

Cloud thickness above the defined threshold typically signals exceeding momentum and can lead to a quick reversal. During these thick periods, if the width exceeds the defined threshold, small triangles mark potential reversal points. In order for the reversal shape to show, the color of the cloud has to be the opposite. So, for example, if the cloud is bearish, and exceeds momentum, defined by the user, a bullish signal appears. The opposite conditions for a bullish signal. This approach can help traders focus on notable changes rather than minor oscillations.

🟪 Bar Coloring and Layered Lines

Bars take on bullish or bearish tints, matching the faster line’s position relative to the slower line. The lines themselves are plotted multiple times with varying opacities, creating a layered, glowing look that enhances visibility without affecting calculations.

🟩 The Metrics Table

Located in the top-right corner of the chart, this table displays:

• SMA1 and SMA2 current values.

• Bullish or bearish alignment for each line.

• Cloud thickness.

• Reversal zone status (in or out of zone).

This numeric readout allows for a quick data check without hovering over the chart.

🟪 Why These Specific Moving Average Lengths Are Used

Default lengths of 14, 28, and 50 are common in technical analysis. Fourteen captures near-term price movement without overreacting. Twenty-eight, roughly double 14, provides a moderate smoothing level. Fifty is widely regarded as a medium-term benchmark. Multiplying each length by 1.5 for the slower line enhances separation when combined with the faster line.

🟩 Originality and Usefulness

• Multi-Layered Smoothing. The user can select from several moving average modes, including a unique “optimized” blend, possibly reducing random fluctuations in the market data.

• Combined Visual and Numeric Clarity. Bars, clouds, and a real-time table merge into a single interface, enabling efficient trend analysis.

• Focus on Significant Shifts. Thick cloud zones and triangles draw attention to potentially stronger momentum changes and plausible reversals.

• Flexible Across Markets. The adjustable lengths and threshold can be tuned to different asset classes (stocks, forex, commodities, crypto) and timeframes.

By integrating multiple technical concepts—cloud-based trend detection, color coding, reversal markers, and an immediate reference table—the Uptrick Signal Density Cloud aims to streamline chart reading and decision-making.

🟪 Additional Considerations

• Timeframes. Intraday, daily, and weekly charts each yield different signals. Adjust the smoothing lengths and threshold to suit specific trading horizons.

• Market Types. Though applicable across asset classes, parameters might need tweaking to address the volatility of commodities, forex pairs, or cryptocurrencies.

• Confirmation Tools. Pairing this indicator with volume studies or support/resistance analysis can improve the reliability of signals.

• Potential Limitations. No indicator is foolproof; sudden market shifts or choppy conditions may reduce accuracy. Cautious position sizing and risk management remain essential.

🟩 Disclaimers

The Uptrick Signal Density Cloud relies on historical price data and may lag sudden moves or provide false positives in ranging conditions. Always combine it with other analytical techniques and sound risk management. This script is offered for educational purposes only and should not be considered financial advice.

🟪 Conclusion

The Uptrick Signal Density Cloud blends trend identification, momentum assessment, and potential reversal alerts in a single, user-friendly tool. With customizable smoothing methods and a focus on cloud thickness, it visually highlights important market conditions. While it cannot guarantee predictive accuracy, it can serve as a comprehensive reference for traders seeking both a quick snapshot of the current trend and deeper insights into market dynamics.

Internals Elite NYSE [Beta]Overview:

This indicator is designed to provide traders with a quick overview of key market internals and metrics in a single, easy-to-read table displayed directly on the chart. It incorporates a variety of metrics that help gauge market sentiment, momentum, and overall market conditions.

The table dynamically updates in real-time and uses color-coding to highlight significant changes or thresholds, allowing traders to quickly interpret the data and make informed trading decisions.

Features:

Market Internals:

TICK: Measures the difference between the number of stocks ticking up versus those ticking down on the NYSE. Green or red background indicates if it crosses a user-defined threshold.

Advance/Decline (ADD): Shows the net number of advancing versus declining stocks on the NYSE. Color-coded to show positive, negative, or neutral conditions.

Volatility Metrics:

VIX Change (%): Displays the percentage change in the Volatility Index (VIX), a key gauge of market fear or complacency. Color-coded for direction.

VIX Price: Displays the current VIX price with thresholds to indicate low, medium, or high volatility.

Other Market Metrics:

DXY Change (%): Percentage change in the US Dollar Index (DXY), indicating dollar strength or weakness.

VWAP Deviation (%): Percentage of stocks above VWAP (Volume Weighted Average Price), helping traders assess intraday buying and selling pressure.

Asset-Specific Metrics:

BTCUSD Change (%): Percentage change in Bitcoin (BTC) price, useful for monitoring cryptocurrency sentiment.

SPY Change (%): Percentage change in the S&P 500 ETF (SPY), a proxy for the overall stock market.

Current Ticker Change (%): Percentage change in the currently selected ticker on the chart.

US10Y Change (%): Percentage change in the yield of the 10-Year US Treasury Note (TVC:US10Y), an important macroeconomic indicator.

Customizable Appearance:

Adjustable text size to suit your chart layout.

User-defined thresholds for key metrics (e.g., TICK, ADD, VWAP, VIX).

Dynamic Table Placement:

You can position the table anywhere on the chart: top-right, top-left, bottom-right, bottom-left, middle-right, or middle-left.

How to Use:

Add the Indicator to Your Chart:

Apply the indicator to your chart from the Pine Script editor in TradingView.

Customize the Inputs:

Adjust the thresholds for TICK, ADD, VWAP, and VIX according to your trading style.

Enable or disable the metrics you want to see in the table by toggling the display options for each metric (e.g., Show TICK, Show BTC, Show SPY).

Set the table placement to your preferred position on the chart.

Interpret the Table:

Look for color-coded cells to quickly identify significant changes or breaches of thresholds.

Positive values are typically shown in green, negative values in red, and neutral/insignificant changes in gray.

Use metrics like TICK and ADD to gauge market breadth and momentum.

Refer to VWAP deviation to assess intraday buying or selling pressure.

Monitor the VIX and US10Y changes to stay aware of macroeconomic and volatility shifts.

Incorporate Into Your Strategy:

Use the indicator alongside technical analysis to confirm setups or identify areas of caution.

Keep an eye on correlated metrics (e.g., VIX and SPY) for broader market context.

Use BTCUSD or DXY as additional indicators of risk-on/risk-off sentiment.

Ideal Users:

Day Traders: Quickly gauge intraday market conditions and momentum.

Swing Traders: Identify broader sentiment shifts using metrics like ADD, DXY, and US10Y.

Macro Investors: Stay updated on key macroeconomic indicators like the 10-Year Treasury yield (US10Y) and the US Dollar Index (DXY).

This indicator serves as a comprehensive tool for understanding market conditions at a glance, enabling traders to act decisively based on the latest data.

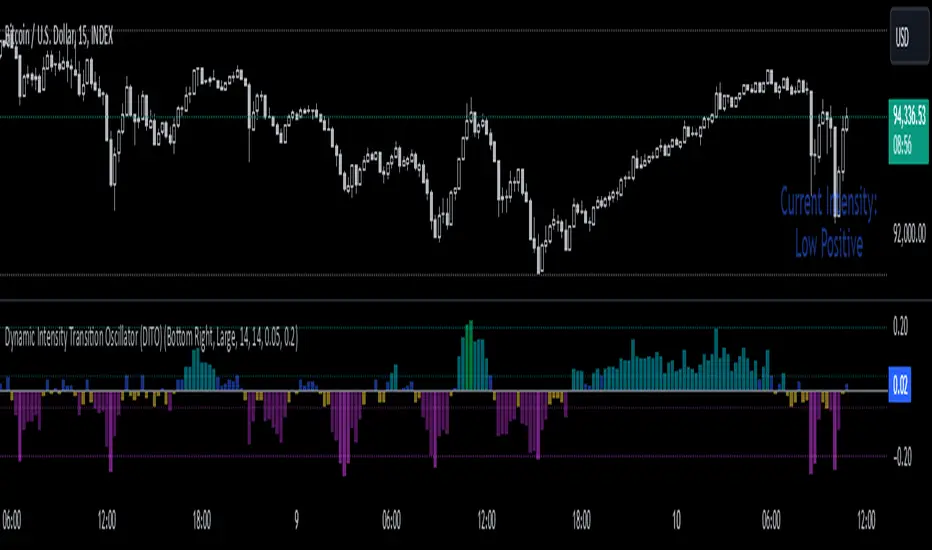

Dynamic Intensity Transition Oscillator (DITO)The Dynamic Intensity Transition Oscillator (DITO) is a comprehensive indicator designed to identify and visualize the slope of price action normalized by volatility, enabling consistent comparisons across different assets. This indicator calculates and categorizes the intensity of price movement into six states—three positive and three negative—while providing visual cues and alerts for state transitions.

Components and Functionality

1. Slope Calculation

- The slope represents the rate of change in price action over a specified period (Slope Calculation Period).

- It is calculated as the difference between the current price and the simple moving average (SMA) of the price, divided by the length of the period.

2. Normalization Using ATR

- To standardize the slope across assets with different price scales and volatilities, the slope is divided by the Average True Range (ATR).

- The ATR ensures that the slope is comparable across assets with varying price levels and volatility.

3. Intensity Levels

- The normalized slope is categorized into six distinct intensity levels:

High Positive: Strong upward momentum.

Medium Positive: Moderate upward momentum.

Low Positive: Weak upward movement or consolidation.

Low Negative: Weak downward movement or consolidation.

Medium Negative: Moderate downward momentum.

High Negative: Strong downward momentum.

4. Visual Representation

- The oscillator is displayed as a histogram, with each intensity level represented by a unique color:

High Positive: Lime green.

Medium Positive: Aqua.

Low Positive: Blue.

Low Negative: Yellow.

Medium Negative: Purple.

High Negative: Fuchsia.

Threshold levels (Low Intensity, Medium Intensity) are plotted as horizontal dotted lines for visual reference, with separate colors for positive and negative thresholds.

5. Intensity Table

- A dynamic table is displayed on the chart to show the current intensity level.

- The table's text color matches the intensity level color for easy interpretation, and its size and position are customizable.

6. Alerts for State Transitions

- The indicator includes a robust alerting system that triggers when the intensity level transitions from one state to another (e.g., from "Medium Positive" to "High Positive").

- The alert includes both the previous and current states for clarity.

Inputs and Customization

The DITO indicator offers a variety of customizable settings:

Indicator Parameters

Slope Calculation Period: Defines the period over which the slope is calculated.

ATR Calculation Period: Defines the period for the ATR used in normalization.

Low Intensity Threshold: Threshold for categorizing weak momentum.

Medium Intensity Threshold: Threshold for categorizing moderate momentum.

Intensity Table Settings

Table Position: Allows you to position the intensity table anywhere on the chart (e.g., "Bottom Right," "Top Left").

Table Size: Enables customization of table text size (e.g., "Small," "Large").

Use Cases

Trend Identification:

- Quickly assess the strength and direction of price movement with color-coded intensity levels.

Cross-Asset Comparisons:

- Use the normalized slope to compare momentum across different assets, regardless of price scale or volatility.

Dynamic Alerts:

- Receive timely alerts when the intensity transitions, helping you act on significant momentum changes.

Consolidation Detection:

- Identify periods of low intensity, signaling potential reversals or breakout opportunities.

How to Use

- Add the indicator to your chart.

- Configure the input parameters to align with your trading strategy.

Observe:

The Oscillator: Use the color-coded histogram to monitor price action intensity.

The Intensity Table: Track the current intensity level dynamically.

Alerts: Respond to state transitions as notified by the alerts.

Final Notes

The Dynamic Intensity Transition Oscillator (DITO) combines trend strength detection, cross-asset comparability, and real-time alerts to offer traders an insightful tool for analyzing market conditions. Its user-friendly visualization and comprehensive alerting make it suitable for both novice and advanced traders.

Disclaimer: This indicator is for educational purposes and is not financial advice. Always perform your own analysis before making trading decisions.

Average Price Range Screener [KFB Quant]Average Price Range Screener

Overview:

The Average Price Range Screener is a technical analysis tool designed to provide insights into the average price volatility across multiple symbols over user-defined time periods. The indicator compares price ranges from different assets and displays them in a visual table and chart for easy reference. This can be especially helpful for traders looking to identify symbols with high or low volatility across various time frames.

Key Features:

Multiple Symbols Supported:

The script allows for analysis of up to 10 symbols, such as major cryptocurrencies and market indices. Symbols can be selected by the user and configured for tracking price volatility.

Dynamic Range Calculation:

The script calculates the average price range of each symbol over three distinct time periods (default are 30, 60, and 90 bars). The price range for each symbol is calculated as a percentage of the bar's high-to-low difference relative to its low value.

Range Visualization:

The results are visually represented using: